-

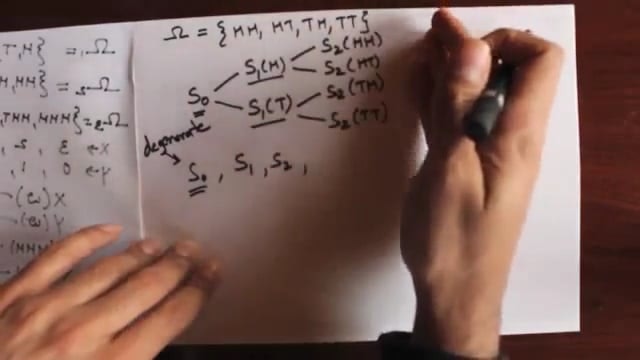

101 - Random Variables

Describes Finite Sample Space and constructs various random variables on that space

-

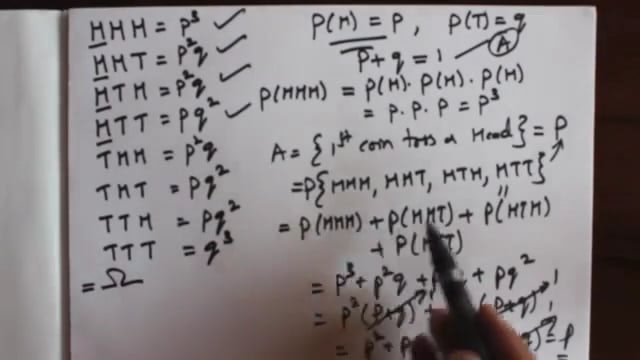

102 - Finite Probability Space

Describes Probability Space and Probability Measure

-

103 - Probability Distribution

Explains Probability Distribution of a Random Variable

-

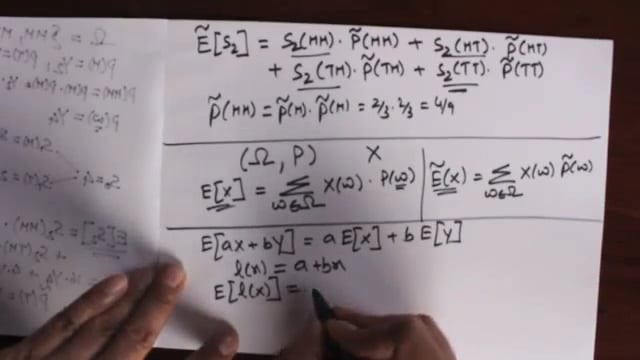

104 - Expectations

Discusses expectation of a random variable under different probability measures

-

105 (a) - Conditional Expectations

Describes conditional expectation of a random variable in a coin toss space

-

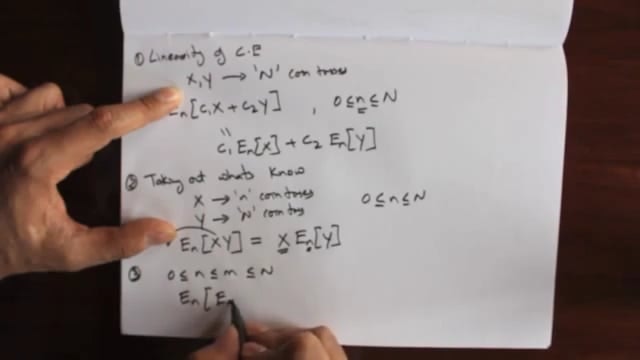

105 (b) - Properties of Conditional Expectations

Discusses properties of conditional expectations.

-

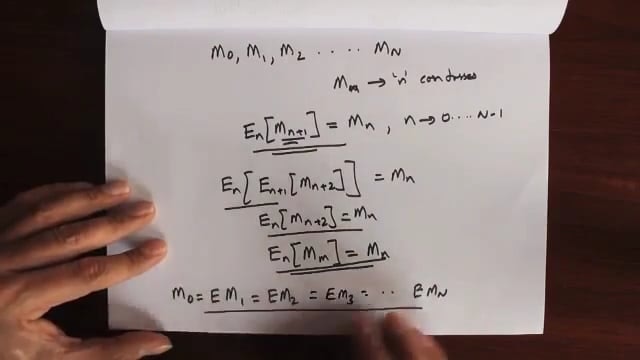

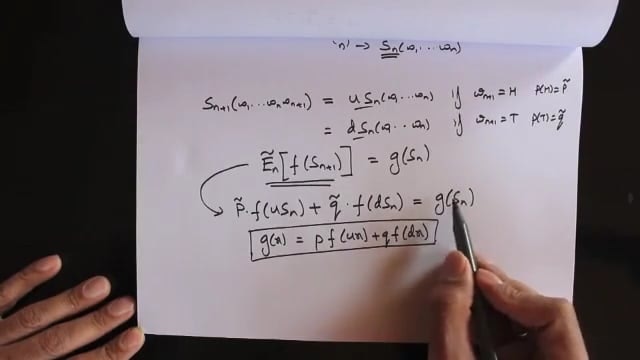

106 (a) - Martingales

Describes a martingale process

-

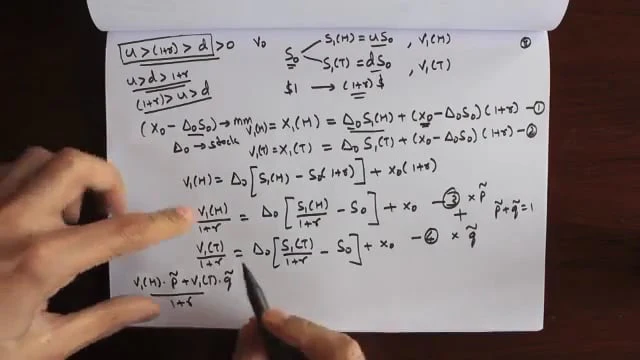

106 (b) - No Arbitrage Pricing Theory

Describes No Arbitrage Pricing in a single period binomial model

-

106 (c) - Risk Neutral Valuation

Describes risk neutral pricing formula in a single period binomial model

-

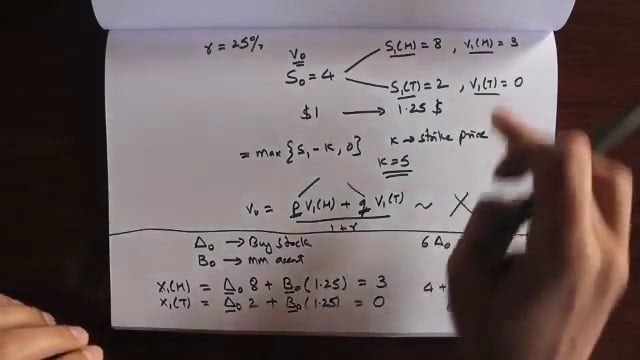

106 (d) - Example of Risk Neutral Valuation

Calculates value of an European Call option using risk neutral formula

-

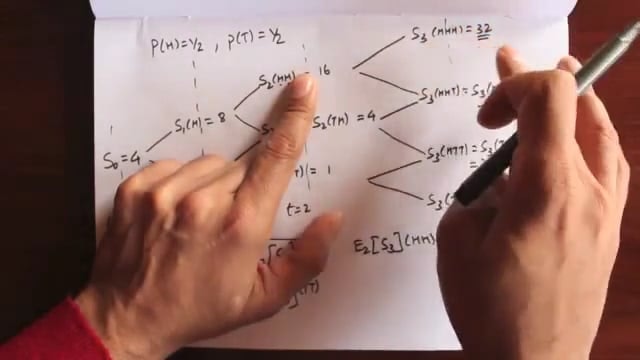

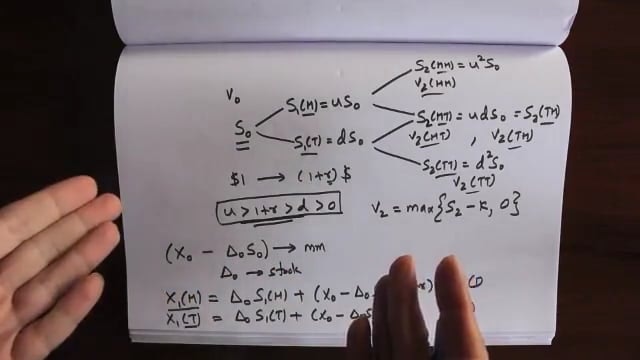

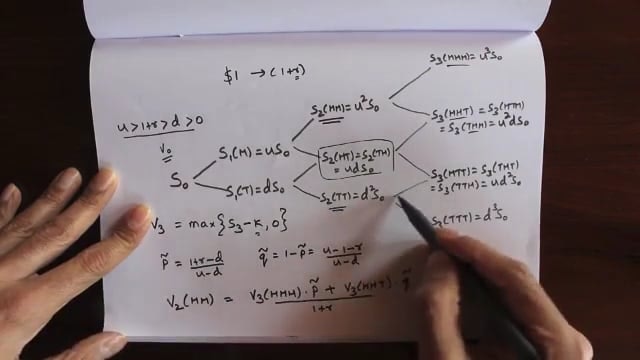

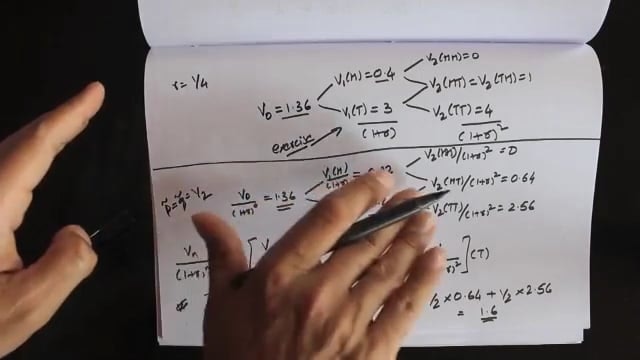

106 (e) - Risk Neutral Valuation in 2 Period Binomial Model

Describes Risk Neutral Valuation in 2 Period Binomial Model

-

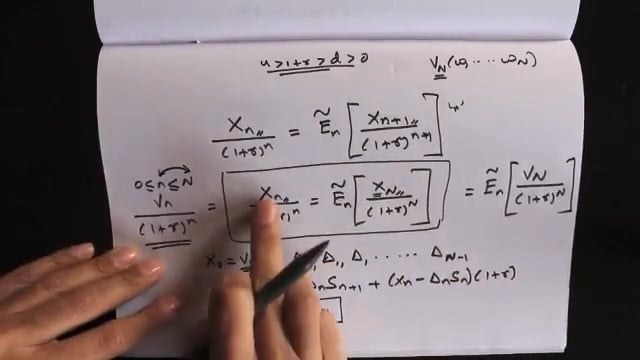

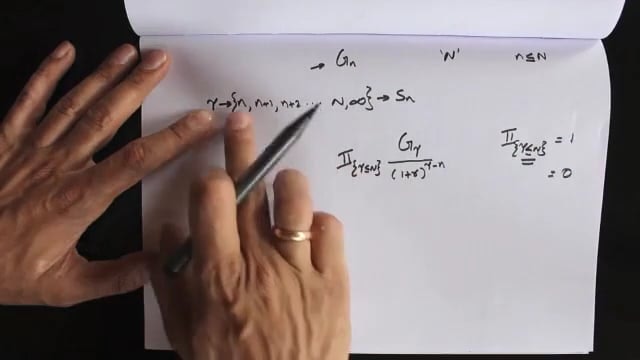

106 (f) - Dynamic Replication in N-Period Binomial Model

Describes how to create a replicating portfolio in N-Period Binomial Model

-

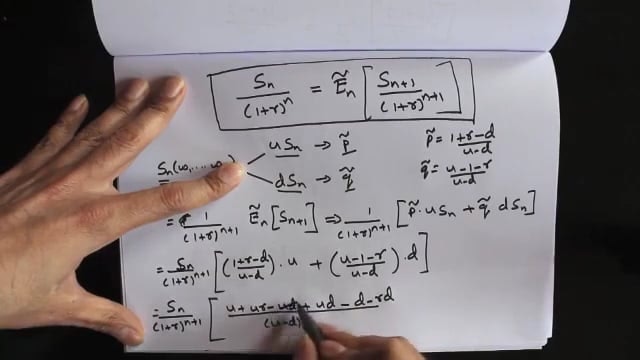

107 - Risk Neutral Measure and No Arbitrage

Describes how to guarantee no arbitrage in a binomial model

-

108 - Cash Flow Valuation

Describes how to value multiple cash flows in a binomial model.

-

109 (a) - Change of Measure- Radon Nikodym Derivative

Describes change of measure using Radon Nikodym Derivative

-

109 (b) - Change of Measure- State Prices

Describes State Prices and State Price Densities

-

109 (c) - Change of Measure- Radon Nikodym Derivative Process

Describes Radon Nikodym Derivative Process

-

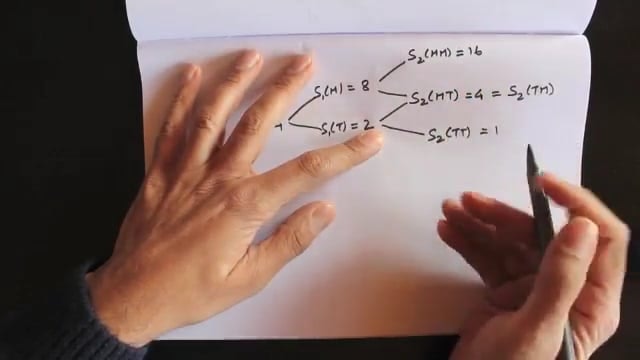

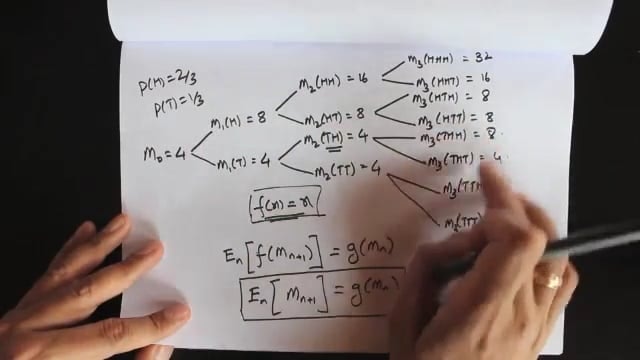

110 (a) - Markov Process

Describes the Markov Process in a Binomial Model Setting

-

110 (b) - Multidimensional Markov Process

Describes Markov Property for Multidimensional adaptive process

-

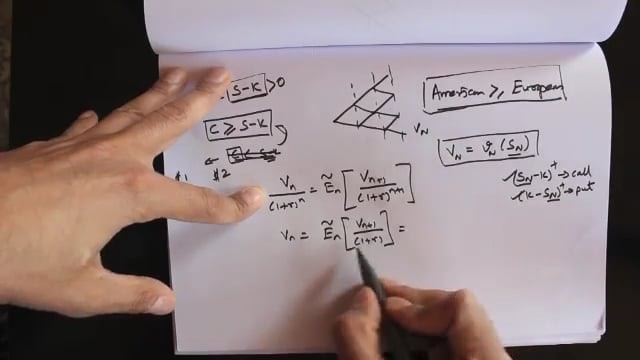

111 (a) - American Derivatives- Non-Path Dependent

Describes how to value Non-Path Dependent American Derivatives using a Binomial Model

-

111 (b) - American Derivatives- Stopping Time

Describes Stopping Time & Stopped Process

-

111 (c) - General American Derivatives

Describes the pricing formula for General American Derivatives